(**) Disclosure: This post may contain affiliate links, meaning RealEstateCareerHQ.com will get a commission if you decide to make a purchase through the links, but at no additional cost to you.

Since I started writing for this website, I made valuable connections with many appraisers through several social media channels. Sometime, I would come across appraisers where their biography would say they are approved to conduct a VA appraisal. I have written about FHA appraisal, farm appraisal, relocation appraisal, and many others, but I really don’t know much about a VA appraisal. So I did some research on this topic and would like to share what I found with you.

What is a VA appraisal? VA appraisal is an assessment report of a subject property, and it is required when obtaining a VA loan. It must be conducted by a qualifying appraiser who is approved by the Department of Veterans Affairs.

Unlike the process of getting a typical mortgage, the lenders do not order the appraisal directly from the real estate appraiser. Instead, they would submit the appraisal request through the Veteran Administration’s online portal. Then VA would assign the appraisal order to the appraisers on their roster.

In this article, you’ll learn the requirement of a VA appraisal, the appraisal fee in different states, its turnaround time, and other cool facts about VA appraisals. So without further ado, let’s get started!

Some Background about VA Loans

To give you a bit of background, VA stands for Veterans Affairs. Some veterans want to purchase a property but are unable to get a mortgage from a conventional lender. This ineligibility could be due to lack of down payment, or poor credit score. To address this issue, the U.S government introduced a financing program called the “VA Home Loan.” The mortgage is still financed by private lenders, but it is guaranteed by the U.S. Department of Veterans Affairs (VA).

Since this creates a large cushion of safety net for lenders, they are more willing to lending out the money. The VA loan is a tremendous help to many military personnel and their families.

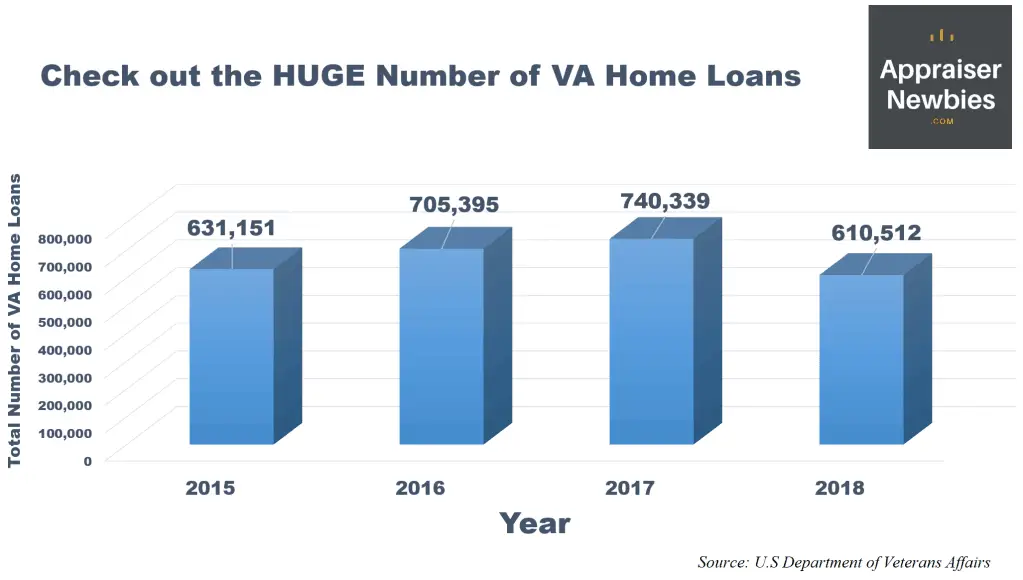

VA Home Loans indeed provide a massive opportunity to the real estate industry. In 2018, the total VA loan amount were $161,295,413,406!

However, not every subject property could qualify for a VA loan. The borrowing amount must be justified by the value in a VA appraisal.

What is the Requirement for a VA Appraisal?

For a property to qualify for a VA loan, it must meet the Minimum Property Requirements (MPR) as outlined in the Department of Veterans Affair’s Compliance Inspector Guide.

There are four main areas you need to look into, which are Property Access, Property Characteristics, Defective Conditions, Other Hazards.

1) Property Access

- The subject property must have access to the public or private street. (Think about it, even when the house is on fire, there needs to be a way firefighters can enter the home.)

- Access should not require you to trespass another property. (Else there could be legal issues all the time)

- There must be adequate space in between buildings for exterior wall maintenance.

2) Property Characteristics

Entity: Since the subject property is the collateral against the VA loan, it needs to be readily marketable.

Usage: The house must be for primarily residential purpose. The rules do allow a portion of the property for non-residential use, but it can’t be more than 25% of the total gross floor area.

So allocating a room to be home office might work, but the VA loan is definitely not for purchasing a commercial office unit.

Living Area and Facilities: The unit cannot be overly small. It must have adequate space for suitable living, cooking, dining, and sleeping.

However, the guide does not specifiy the required dwelling size or the number of rooms required. So you probably need to use your own judgement on that.

I have written another article about “What makes a room a bedroom?” In there, you could find the bedroom size requirement according to the International Residential Code. Perhaps, this could give you some idea of what constitutes an adequate living space for a unit.

As for the facilities, there needs to be sanitation such as a toilet, sink, and bathroom. Amenities such as laundry, storage, and heating can be shared in a 2-4 units building.

Sanitary Facilities, Sewage, and Septic: There must be a safe sewage system in place. It needs to be connected to a public sewer whenever feasible. In some cases, individual and community disposal system could be permitted, but it must be operating properly and meeting the standard of the local health authority or the U.S. Public Health Service.

Utilities: Each unit must have independent services (i.e., water, sewer, gas, electricity). However, if the units are all under the same ownership, they may share the utilities, but only given there are separate shutoffs.

Mechanical Systems: They must be safe to operate, protected from destructive elements, and have quality with a reasonable future lifespan. (If you were the one securing the loan, I’m sure you wouldn’t want the mechanic of the house to be falling apart.)

Heat: Certain parts of the country are extremely cold during the winter. It is necessary to have a heating system to live comfortably and healthfully.

If the home is using a woodburning stove to be the primary heat source, then there must also be a conventional system which could maintain a minimum of 50-degree temperature in the plumbing areas.

However, I have tested 50 °F in my home, and it is still too cold for anyone to stay there for long. In the article that I mentioned earlier, “What makes a room a bedroom?”, the IRC guideline would require a bedroom to maintain at least 68 °F.

More and more homeowners are supporting the green initiatives, so some are using the solar system as their primary heat/hot water source. You could still do that for a VA loan, but there must be a backup system that can provide 100% equivalent utility.

Electricity: The property must have adequate electricity for essential equipment. (i.e., lighting)

Water: The house must have drinkable water. Its quality needs to meet the standard of the local health authority. If there’s no such authority, then it would follow the EPA guidelines.

Of course, the supply of hot water is also essential, you don’t want to take a cold shower during the winter.

Crawl Space and Attics: These areas can build up mold easily. Therefore, there must be natural ventilation to prevent excess moisture and heat. Any ponding of water and debris must be fixed.

Roof: It must have the quality to prevent moisture in entering the house with a minimum remaining lifespan of five years. I have seen some homeowners tried to do a quick fix, so they put several layers of shingles over a defective roof. However, the rules do not permit this practice, so all old shingles with three or more layers would need to be removed.

3) Defective Conditions

Site: Unless you want to live in a water park, the site needs to have a drainage system. It must be properly graded so that the water could flow away from the dwelling.

Although it does not specify in the guide, most houses would have a drainage pipe to prevent water from ponding. But it must extend long enough away from the property.

Furthermore, to prevent erosion, the ground cover must be stabilized.

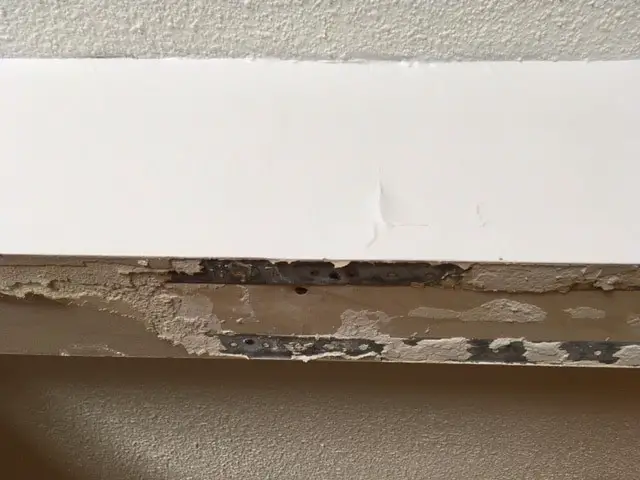

Improvements: When a subject property has conditions which impact its safety, sanitation, or structural soundness, then they must be properly fixed to prevent further damage. (i.e., Defective construction, water leakage, poor workmanship, excessive dampness, decay, continuing settlement, and termites problem).

Here are some common real-life examples, for instance – exposed electric wiring, peeling paint, roof leaks, broken windows, rotted exterior wood trim, plumbing leaks, fungus growth, and dry rot.

Here’s a window trim that needs some fixture

Lead-Based and Defective Paint: Some older houses are using lead-based paint, which could cause health issues. They are especially common for homes built before 1978. If there is Defective Paint problem to those older houses, (i.e., cracking, peeling or loose paint), then they must be corrected.

For properties that were built after 1978, the defective paint problem would only need to be addressed if it poses any safety threat.

4) Other Hazards

Since this session talks about the safety issue, I want to be more careful to ensure there is no misunderstanding in my interpretation. Therefore, I’ll directly quote from the guide so that you could read the exact wording.

Onsite: The property must be free of hazards (such as subsidence or flood or erosion problems) which may adversely affect the health and safety of the occupants, the structural soundness of the improvements, or which may impair the customary use and enjoyment of the property by the occupants.

Offsite: High Voltage Electric Transmission Lines and Gas and Petroleum Pipelines: The dwelling structure must be located outside of the easement area(s). Other onsite improvements can be located in the easement area(s). If a Proposed Construction Dwelling is located outside the Pipeline easement but less than 220 yards away from the centerline, additional conditions apply.

Quote from the Department of Veterans Affair’s Compliance Inspector Guide.

VA Appraisal Checklist [Info-graphic]

How Much Does a VA Appraisal Cost?

VA appraisal costs could range from $450 to $800, and they vary among states.

Real estate appraiser could request additional fees due to its location or complexity, but they need to obtain prior approval from the RLC. The milage rate will be based on the ones listed on the General Services Administration (GSA). Some states could allow an additional $150 for re-inspection fee.

The appraisal fee is usually paid upfront by the person who is requesting the mortgage or refinances. However, one could negotiate with the lenders or sellers whether the appraisal fee could be reimbursed as part of the closing costs.

How Long is the Turnaround Time for a VA appraisal?

The timeline for a VA appraisal is 10 business days on average. The VA appraisal needs to be reviewed by either a VA staff appraiser or a Staff Appraisal Reviewer (SAR) that is employed by the lender.

However, lenders that do not focus on VA lending might not hire SARs. Therefore, they would need to submit the appraisal directly to the VA for further review.

On a side topic, I wrote another article about Review Appraisal, which is a huge part of a SAR’s day-to-day responsibility.

Detailed Chart – VA Appraisal Fees and Turnaround Time in Different States

The following chart applies to Single Family Residence.

| VA Appraisal Fees | Turnaround Time (in Business Days) | |

|---|---|---|

| Alabama | $450 | 5 |

Alaska | $800 | 12 to 15 |

| Arkansas | $500 to $575 | 10 |

Arizona | $600 | 7 to 10 |

| California | $600 | 7 to 10 |

| Colorado | $750 | 10 |

| Connecticut | $525 | 10 |

| Delaware | $550 | 10 |

| Florida | $450 | 5 |

| Georgia | $450 | 7 |

| Hawaii | $600 to $700 | 10 to 15 |

| Idaho | $600 | 7 |

| Indiana | $525 | 5 |

| Illinois | $450 | 10 |

| Iowa | $450 | 10 |

| Kansas | $450 to $500 | 10 |

| Kentucky | $475 | 10 |

| Louisiana | $500 to $600 | 10 |

| Maine | $675 | 10 |

| Maryland | $525 | 10 |

| Massachusetts | $525 | 10 |

| Michigan | $525 to $600 | 5 |

| Minnesota | $450 | 10 |

| Mississippi | $450 | 5 |

| Montana | $800 to $900 | 28 |

| Nebraska | $475 to $525 | 10 |

| Nevada | $600 | 10 to 15 |

| New Hampshire | $550 | 10 |

| New Jersey | $525 | 5 |

| New Mexico | $600 | 7 to 15 |

| New York | $525 | 10 |

| North Cariolina | $525 to $575 | 7 |

| North Dakota | $625 to $675 | 15 |

| Ohio | $525 | 5 |

| Oregon | $800 | 14 |

| Pennsylvania | $525 | 5 |

| Rhode Island | $525 | 5 |

| South Carolina | $425 | 7 |

| South Dakota | $500 to $575 | 15 |

| Texas | $500 to $700 | 10 |

| Tennessee | $500 to $575 | 7 |

| Vermont | $650 | 10 |

| Virginia | $525 | 10 |

| Washington | $800 | 14 |

| West Virginia | $575 | 10 |

| Virgin Island | $675 | 5 |

| Wyoming | $600 | 7 to 14 |

| Wisconsin | $450 | 10 |

| Utah | $600 | 7 |

Source: US Department of Veterans Affairs website

Can VA Appraisal be Transferred to Another Lender?

Yes, if a VA case number already exists with another lender, then an appraisal transfer request can be submitted to them. Usually, an assignment fee would be involved.

However, if the appraisal was incomplete or canceled by the previous lender, then a new VA appraisal must be done.

Related Questions

1) Does a VA appraisal follow the property?

Yes, the VA appraisal would follow the property and be in the system for six months. However, this would only impact the VA loan application.

2) How to become a VA appraiser?

To become a VA appraiser, you need to maintain the residential appraiser license in the state you are providing the services. You’ll need at least five years of experience in appraising for residential properties.

Conclusion

Despite there is such a massive volume of VA loans every year, there is a lack of VA appraisers in recent years. Some home sellers may opt for non-VA buyers due to this reason.

Working on VA appraisals not only is a great way to expand your scope of practice, but you are also providing a valuable service to the veteran community.

So that’s all I have to share for now and I hope you enjoy this article. Is there anything about VA appraisals that you want to share? If so, please leave us a comment below.

The first step to your appraisal career is to complete the pre-licensing courses from a trusted education provider. McKissock received an incredible rating from its students, and their online lessons are taught by instructors who have actual experience in the appraisal industry. You may click here to find out more about their courses. (**)

(**) Affiliate Disclosure: Please note that some of the links above are affiliate links, and at no additional cost to you. Our company, JCHQ Publishing will earn a commission if you decide to make a purchase after clicking on the link. Please understand that we include them based on our experience or the research on these companies or products, and we recommend them because they are helpful and useful, not because of the small commissions we make if you decide to buy something through the links. Please do not spend any money on these products unless you feel you need them or that they will help you achieve your goals.

Disclaimer: The information in this post is for general information only, and not intend to provide any advice. They are subjected to change anytime without notice, and not guaranteed to be error-free. For full and exact details, please contact the Appraisal Board in your state, the education or service provider.

Reference:

- US Department of Veterans